Archive for category Financial Services

SEC Clears Social Media for Use: What does it mean?

Posted by ASocialNomad in Actiance, eDiscovery, Enterprise 2.0, Facebook, Financial Services, Google, LinkedIn, personal v professional, Retail banking, Securities and Exchange Commission, Social Networking, Trends on April 16, 2013

On April 2nd the SEC issued a press release, which has been widely reported in a number of ways, as to what this actually means for organizations. In this blog, lets take a look at what it actually means.

On April 2nd the SEC issued a press release, which has been widely reported in a number of ways, as to what this actually means for organizations. In this blog, lets take a look at what it actually means.

WHAT DOES THE SEC SAY?

Here’s what the SEC actually says “companies can use social media outlets like Facebook and Twitter to announce key information in compliance with Regulation Fair Disclosure (Regulation FD) so long as investors have been alerted about which social media will be used to disseminate such information”.

The exact text is on the SEC website: http://www.sec.gov/news/press/2013/2013-51.htm We’re pleased to see that the content was tweeted as well. Interestingly, it was in 2008 that the SEC actually cleared the use of websites for the dissemination of key information. It feels like its been a long five years to get the same clearance for social media. But perhaps not. On August 6th 1991, some 17 years earlier the first website was born, at CERN – the first URL for that website was http://info.cern.ch/hypertext/WWW/TheProject.html in case you want to check it out. So, it appears progress is being made. Our world is speeding up.

WHAT DOES THAT ACTUALLY MEAN?

- It means that, so long as a public company announces in advance, what social outlets they will use, that they are able to disseminate key information through these channels.

- In general, key information is usually mailed out or put on a wire service like Marketwire or PR Newswire and also onto the company website.

DOES THIS MEAN THAT THE FINANCIAL SERVICES INDUSTRY WILL NOW ALL BE ON SOCIAL?

- Not necessarily, it doesn’t meant that individuals in companies will necessary be all now posting content through their individual network updates.

- It does mean that firms will need to open up access to social media so that Financial Advisers, Relationship Managers and those assisting clients with investment information can access this information – it really IMO opens the floodgates for firms now saying, that if you have financial professionals who need to keep up to date with key publicly traded companies, then they need to see this information. If you don’t, then it would be like forbidding a professional to read the newspaper or watch TV.

- Usually when public companies distribute key information like this, they distribute it through a “corporate property” – in social terms this would be the company Facebook page, or the company Twitter account, or the company page on LinkedIn.

- Record retention requirements means that companies will have retain records of what they posted. i.e. LinkedIn company updates.

WHAT DOES IT MEAN TO THE DISTRIBUTED TEAM?

- It means that they will require access to social in order to conduct their work effectively.

- As a result of the SEC’s ruling, anyone that needs to keep an eye on key information from public companies will NEED to have access to social in order to remain competitive.

- The socially savvy public company will use individuals to push this content out, along with corporate brands. Take Reed Hastings of Netflix for instance – this whole thing started because it was HIS Facebook page, not the company page.

WHAT DOES IT MEAN TO FINANCIAL SERVICES FIRMS and PUBLIC COMPANIES?

1) Archiving company updates for public companies will become a must have. Public companies will need to archive the company updates and any other updates that are related to Regulation FD.

2) Ensuring that the right person / people approved this content is key. They will need to prove that it was approved by the relevant individuals/groups in the organization.

3) Companies may choose to share content to a “Shareholders Group” on LinkedIn, a group on Facebook, or a private feed on Twitter, thus requiring that content is approved and archived, is again key.

4) Some companies might select individuals to share this key information – so ensuring that the content is again approved and archived is key. However, the SEC points out, that “The report of investigation explains that although every case must be evaluated on its own facts, disclosure of material, nonpublic information on the personal social media site of an individual corporate officer — without advance notice to investors that the site may be used for this purpose — is unlikely to qualify as an acceptable method of disclosure under the securities laws. Personal social media sites of individuals employed by a public company would not ordinarily be assumed to be channels through which the company would disclose material corporate information.” So ensure prior notification has been made – and that it is clear, which channels and which accounts will be used to disseminate this information.

5) Those firms that block social access for the wider team will not be evaluating their policies, in order to provide open access to at least view for instance LinkedIn news and company updates while on corporate machines.

6) Social networks outside of Facebook and Twitter should be lobbying the SEC – who referenced only Facebook and Twitter – but not LinkedIn as social channels. LinkedIn is the network that most business professionals feel comfortable with and with whom they connect with business colleagues on much more than Facebook and Twitter. It’s clear that the SEC needs to understand the company area of LinkedIn, but also the value of the personal network – using the Reed Hasting’s example – if he had used his LinkedIn network update to push this out, it would have had the same effect as he did with Facebook.

WHAT SHOULD YOU DO?

1) Review your social policies, both for listening, and for distributing content. This great move by the SEC has opened the way for “no business reason for social” to be removed. Ensure that you’re including all the stakeholders into this review.

2) Ensure, if you are a public company, that any content you are sharing on social – goes through the same approvals that content for other mediums does. Archive it and retain it.

3) Embrace this new communications modality approval by the SEC. Those who disseminate key information in compliance with Regulation FD, through social channels, will certainly be in the forefront of the press and generate those softer elements of ROI, that we all strive for. So make sure you take this into consideration when you’re looking at the benefits of social.

Let me wrap up by asking a question. If you were to choose one social channel to share key information.. what would it be?

Belbey Blogs: Recent Guidance from the SEC on Filing Social Media

Posted by belbey in Actiance, Compliance, eDiscovery, Electronically Stored Information (ESI), Enterprise 2.0, Financial Services, FINRA, Securities and Exchange Commission, Uncategorized on April 2, 2013

Today’s blog is from Joanna Belbey, Social Media and Compliance Specialist at Actiance.

This month, the Division of Investment Management of the Securities and Exchange Commission issued the first in a series of “IM Guidance Updates” to clarify its positions on emerging legal issues. The first topic was social media.

Financial services firms are cautious by nature, and its both our experience and no surprise, that firms are taking a very conservative approach and are filing a huge amount of social media content with FINRA. The SEC is calling out that this may be unnecessary in a number of cases.

First some background. To ensure that communications from financial institutions are suitable, fair and balanced, the FINRA Advertising Regulation Department reviews the content of more than 100,000 communications every year. Some communications are submitted as required by FINRA rules, others are submitted voluntarily. Some are filed in advance, others within 10 days of publication. However in FINRA Rule 2210(c)(7)(M), effective February 2013, retail communications posted on an “online interactive electronic forum that is contained on a social media website” are specifically excluded from these filing requirements.

However, as firms have other filing requirements aside from FINRA, such as Section 24(b) of the Investment Company Act of 1940 (“1940 Act”) or Rule 497 under the Securities Act of 1933 (“1933 Act”), SEC has seen fit to provide guidance on what should and should not be filed.

As the SEC states “Whether a communication need be filed depends on the content, context, and presentation of the particular communication”. So nothing changes there. This is simply reiteration. But now the SEC goes a little further. The more specific, the more likely it needs to be filed. And as an aside, whether the communications are filed or not, they still need to captured, supervised, archived, made e-discoverable like any other written communication for “business as such”.

The SEC provided some examples for clarity:

Do Not File

- Simple mention of a specific investment company or family of funds without discussion of merits

- Mention of word “performance” in connection with a specific investment company or family of funds without mention of returns

- Factual introductory statement / hyperlink to fund prospectus (ie, report available here)

- An introductory statement not related to investment merits of a fund that includes hyperlink to general information

- Response to an inquiry via social media that provides factual information and does not include merits of the fund

File (to meet requirements of Section 24(b) or Rule 482):

- Discussion of fund performance that provides specific mention of fund’s returns

- Issuer communications that discuss merits of an investment fund

The regulators continue to reinforce what we know to be best practices of social media. Pitching financial products, and discussing specific performance and returns is unwelcome on social media and may require pre-approval by a registered principal of the firm as well as filing requirements.

A better approach?

Provide compelling content, not sales pitches. Offer information that is informative, entertaining, and worth sharing. In a compliance-constrained industry like financial services, delivering compelling content can be challenging, but it’s by no means impossible.

The first step is to inventory your existing content to see what can be leveraged for social media. Start with pre-approved content that has been reviewed by the company’s compliance team for both corporate governance and regulatory compliance. Use this content to develop a library of interesting insights on investment strategies, wealth management, saving for college or retirement, and similar topics. These articles can provide a foundation for social media newcomers who are looking to start building their online networks.

This Spring is a great time to get started!

Other information you may find helpful:

Belbey Blogs: New FINRA Communications Rule 2210

http://blog.actiance.com/2013/02/13/belbey-blogs-new-finra-communications-rule-2210/

Division of Investment Management of the Securities and Exchange Commission Issues Guidance Update on Social Media Filings by Investment Companies

http://www.sec.gov/news/press/2013/2013-40.htm

IM Guidance Update March 2013

FINRA Rule 2210

http://finra.complinet.com/en/display/display_main.html?rbid=2403&element_id=10648

Regulatory Notice 12-29 Communications with the Public

http://www.finra.org/web/groups/industry/@ip/@reg/@notice/documents/notices/p127014.pdf

Regulatory Notice 10-06, Social Media Web Sites: Guidance on Blogs and Social Networking Web Sites (January 2010)

http://www.finra.org/web/groups/industry/@ip/@reg/@notice/documents/notices/p120779.pdf

Guide to the Web for Registered Representatives

http://www.finra.org/Industry/Issues/Advertising/p006118

FINRA: RCA – March 1999 – Ask the Analust – Electronic Communications

https://www.finra.org/Industry/Regulation/Guidance/RCA/p015326

Belbey Blogs: Are you Ready for Your Social Media Crisis? Consider War Games.

Posted by belbey in Actiance, Employee Behavior, Financial Services on February 25, 2013

Todays’ post is from Joanna Belbey, Social Media and Compliance Specialist, Actiance. @Belbey

Todays’ post is from Joanna Belbey, Social Media and Compliance Specialist, Actiance. @Belbey

We all know that the continued success of any business depends on its reputation. That’s the primary purpose of all our advertising, marketing and public relations campaigns. But what happens when something goes wrong? All that hard work can vanish with one poorly handled crisis.

That’s why most larger firms have Crisis Communications Plans that describe the processes to follow for a number of scenarios. Some of the smarter firms have even created plans just for social media. They recognize that at some point, you can pretty much guarantee that your firm will attract some very public, very unwelcome negative attention. And that social media will just amplify it. In fact, as firms are discovering, social media can actually create the crisis.

Once the plans are approved, most firms cross their fingers and secretly hope that it never happens to them.

However, at a recent Business Development Institute event, I discovered that a few firms actually test their preparedness by conducting “war games”. I was curious how that would work, so after the event, I spoke with the media relations and social media team at a large financial services firm to learn how they did it.

They relayed that when their sales teams began to use social media, they became acutely aware of both the benefit and risk for the organization. So they enlisted their Public Relations Firm of Record to help them test both their traditional and social media crisis communications plans in real time.

Goals:

- Respond appropriately to a crisis in real time, which would involve identifying an issue, making the decision to respond, crafting the response in the right tone, gaining approval of the response, and delivering the response publically across numerous outlets in a timely manner.

- Proactively communicate with various audiences that include: customers, employees, agents, news media, local community, company management, directors and investors, trade associations, government elected officials, regulators and other authorities and suppliers.

- Find the right balance between thoughtfulness and urgency.

Approach:

- Consciously create anxiety to make the test as real and memorable as possible.

- Pick topic in advance.

- Simulation to be cross functional: identify and gather all key stakeholders such as legal, risk, compliance, public relations, marketing, customer service, corporate communications, investor relations, human relations, subject matter experts, senior execs, IT and Security.

- Inform senior management in advance.

- Guarantee no leaks. Create a safe, secure environment by conducting the test off site in controlled environment. In this case, no email was used, all communications among the team were paper-based. Personal electronics were not allowed in the war room during event.

- Test the plans over time. Every 1.5 hours represented a day, as an acute crisis can extend over several days.

- Monitor activities across traditional and social media.

- Respond in real time across multiple outlets to the crisis.

Lessons learned:

- Social media both creates traditional media and adds a level of urgency / responsiveness. Responding to thousands (or hundreds of thousands) of comments across social media is very different that handling incoming phone calls from traditional media.

- Having access to pre-identified subject matter experts with well defined approval processes, allows the ability to craft realistic responses quickly.

- Combining two crisis communications plans (traditional and social media) insures accountability.

And as planned, the test was stressful and memorable. “We’re glad it’s over!” said the participants of the war games for this financial services firm.

But they take comfort in being prepared for an upcoming crisis.

Is your firm ready?

Advisor View: I Believe in Social Media!

Posted by actiance in Financial Services, Guest Post, personal v professional, Social Networking on February 21, 2013

This week’s thought leader Thursday commentary comes from Kim Gaxiola,CFP®, AAMS, Financial Advisor, speaker, educator, and founder of TechGirl Financial. As a big fan of women in technology, Kim’s mission is to provide Silicon Valley with financial education that makes professionals and employees more comfortable making important financial decisions. She has over 10 years of experience as a financial advisor, 15 years in the financial services industry, and a bachelor’s degree in economics from the University of California, Los Angeles (UCLA).

If my husband Victor told me 2 years ago that I was going to have my own blog, and actually enjoy writing articles, posting them on social media, and seeing the response I was going to generate from it, I would have said NO WAY. I have enough to do just managing my practice. Why do I need to write articles, and then tweet, like them, or pass on LinkedIn? I could just pass around others good content.

If my husband Victor told me 2 years ago that I was going to have my own blog, and actually enjoy writing articles, posting them on social media, and seeing the response I was going to generate from it, I would have said NO WAY. I have enough to do just managing my practice. Why do I need to write articles, and then tweet, like them, or pass on LinkedIn? I could just pass around others good content.

It pains me to say it, but he was right! As you can see from this article itself, I am not known for my writing. When I started my new website www.techgirlfinancial.com and included a blog component, I slowly started to include my own material, along with the marketing material I purchased or found on the web. After writing a couple articles and shamelessly promoting them on Facebook, Twitter, and LinkedIn, I have grown to like this aspect of my business. I have found that is very fun to write and get noticed as an authority when it comes to things having to do with personal financial planning and other matters. It is amazing to see how I can reach out to people near and far simply by telling a story and then sharing it using social media.

My website is my unique place to bring content and ideas on topics having to do with financial planning or my niche market, women in technology. My profiles on LinkedIn, Twitter, and Facebook are my amplifiers. It is my voice and my interests that are being shared across the country to my unique audience of women that I like to work with. This is the new medium that delivers the right content to the right audience, and they are looking for your message. If you are not out there telling it to them, they are finding it from someone else. Who do you want them to see, you or someone else?

It is so fascinating to see the “likes” or the activity and “comments” generated from the different posts and material I provide. We don’t always know what resonates with our clients and prospects. The geeky financial articles on the markets are fascinating to me, but they aren’t always what resonate with my clients. Using social media helps me identify those aspects that are more important or interesting to clients and prospects as well. That allows me to send a message and identify with them on a more personal note.

In addition to telling, it’s extremely fun to sit back and listen. Our business is all about helping families reach their goals. This is the core of what individuals are sharing with their friends on Facebook. You will have a much quicker ability to react to life changes when you see them posting on Facebook, then if you were to wait around for them to call you. That’s IF they call you. As I listen and see photos of my clients as they report about the birth of a baby or grandchild, a new job, a wedding, etc…it is with great pleasure that I can witness these happy events with them, and make sure that the proper planning steps are being done at those key life events. There is much to worry or stress about in our business. But this is not it. This is a place where our relationships with our clients can become so much deeper. If you’re not taking advantage of that, you may be missing out. More important, someone else may be listening and connecting on a more personal note than you.

Kim Gaxiola may be reached at (800) 584.3652 or kim@gaxiolafinancialgroup.com or www.techgirlfinancial.com.

TechGirl Financial is a part of Gaxiola Financial Group. Registered representative, securities offered through Cambridge Investment Research, Inc., broker-dealer, member FINRA/SIPC. Investment advisor representative, Cambridge Investment Research Advisors, Inc., a registered investment advisor. Cambridge and Gaxiola Financial Group are not affiliated. Gaxiola Financial Group | 305 Vineyard Town Center #369 | Morgan Hill, CA 95037Belbey Blogs: New FINRA Communications Rule 2210

Posted by belbey in Actiance, Compliance, Financial Services, FINRA, Uncategorized on February 13, 2013

On February 4, 2013, as result of the systematic harmonization of NASD, NYSE and FINRA rules, FINRA Communications with the Rule 2210, went into effect. I wanted to learn more, so I attended the SIFMA Compliance and Legal Society, New FINRA Communications Seminar last week. It was an educational panel that include Kevin Zambrowicz (SIFMA), John Lajiness (Fidelity), Tom Pappas (FINRA), Holly Smith (Sutherland Asbill & Brennam) and Edward Sullivan (UBS).

On February 4, 2013, as result of the systematic harmonization of NASD, NYSE and FINRA rules, FINRA Communications with the Rule 2210, went into effect. I wanted to learn more, so I attended the SIFMA Compliance and Legal Society, New FINRA Communications Seminar last week. It was an educational panel that include Kevin Zambrowicz (SIFMA), John Lajiness (Fidelity), Tom Pappas (FINRA), Holly Smith (Sutherland Asbill & Brennam) and Edward Sullivan (UBS).

The panel discussed that FINRA Rule 2210 brings some significant changes to the communications rule and that firms were expected to update their Written Supervisory Procedures accordingly. However, the rule was announced back in June, so firms have had plenty of time to get ready.

In fact, as Edward Sullivan, Head of Field Compliance at UBS, told the audience, his firm took the new rule as an opportunity to take a fresh look at the communications policies at his firm and make enhancements where appropriate.

So, how does FINRA Rule 2210 impact social media?

First some background. Back when FINRA issued Regulatory Notices 10-06 and 11-39, there were six major categories of communications under the existing NASD Rule 2210.The former six categories (advertisements, sales literature, correspondence, institutional sales material, independently prepared reprints, and public appearances) have now been replaced by three: Correspondence, Retail Communications, and Institutional Communications.

Let’s take a look at the two that impact social media:

Correspondence includes any type of written (including electronic) communication that is distributed or made available to 25 or fewer retail investors within any 30 calendar-day period. Like email, these communications do not require pre-approval, but, firms need to capture, retain and make business communications e-discoverable as well as demonstrate that they are supervising communications to meet suitability requirements. An example from social media might include an InMail on LinkedIn, a Message on Facebook, or a Direct Message on Twitter.

Retail communication includes any written (including electronic) communication that is distributed or made available to more than 25 retail investors within any 30 calendar-day period. A “Retail investor” includes any person other than an institutional investor, regardless of whether the person has an account with the firm. Communications that formerly qualified as advertisements and sales literature generally now fall under the definition of “retail communication.” These communications require pre-approval from a principal of the firm, plus all the record keeping and suitability rules apply. However, the rules specifically exempted pre-review any retail communication that:

- is posted on an online interactive electronic forum

- does not make any financial or investment recommendation or otherwise promote a product or service of the firm.

FINRA recognizes that due to the real time nature of social media, pre-review would inhibit interactive communications. Examples from social media include posts such as LinkedIn Updates, Facebook Status Updates, and Tweets on Twitter.

But, what about static portions of social media like profiles and links to content? Tom Pappas, Thomas A. Pappas, Vice President & Director, Advertising Regulation, FINRA, reiterated that the new rule codified existing guidance from 10-06 and 11-39 and that static portions of social media would still require pre-review unless they are exempted as above. In other words, if static content promotes a product or service, it requires pre-approval.

So, will this significantly change processes around social media? Probably not. As I mentioned in my blog, Belbey Blogs: What Are Other Firms Doing?, we have found that firms tend to pilot social media with pre-approval of all initial posts (such as tweets) and keep tight controls in place. Registered persons typically don’t have much latitude. However, once they begin to trust technology to safeguard their firms’ reputation and stay compliant, firms often begin to allow their reps to personalize content to varying degrees.

It just takes time. And some successes to accelerate the process.

For more information, see:

Full text of Communications Rules (32 pages)

FINRA Regulatory Notice 12-29 Communications with the Public (25 pages)

When the social party grows up, what if no one attends?

Posted by belbey in Actiance, Collaboration, Compliance, eDiscovery, Employee Behavior, Enterprise 2.0, Financial Services, FINRA, New Internet, Social Networking, Trends on February 6, 2013

Today’s post is a collaboration between Richie Etwaru, Director, UBS and Joanna Belbey, Social Media and Compliance Specialist, Actiance

Our last blog, “Before You Go Social, Check with Uncle Sam” covered the regulatory compliance, corporate governance, and legal requirements organizations must address before deploying social collaboration, or “internal social media.” In short, we suggested firms needed to develop policies and deploy or procure intelligent software to automate the capture, archive, retain, and supervise business communications across the enterprise.

We received material feedback. Readers reminded us that we’ve all been having the “compliance and technology conversation” around social media for some time. We aim to please so asked what’s next; we were told adoption is the biggest barrier to success. How do you make the changes to the corporate DNA to allow collaboration to flourish? In other words, how do you get adoption?

Apparently there is a party happening on grown up social networks but no one is attending.

Solving for Adoption

At the core of the thought leadership, we must look at training, sponsorship and design as three individual agendas solving for adoption. The diagram below shows three audiences for each agenda in a 3X3 matrix. The 3X3 matrix can serve as a maturity model as an organization progresses from top right of the matrix to bottom left.

Training, no one flyer fits all

There is no “one size fits all” training for employees to learn how to be “social” within the enterprise. At the one end of the audience spectrum, are employees who are adept at using social media in their personal lives. These are usually (but not always) entry-level employees. They may freely share personal experiences and thoughts with hundreds (thousands?) of their friends on Facebook or followers on Twitter. This set of employees may need to learn how to be “professionally social” within a corporate environment. There is unlearning, think first, and when in doubt resist, training needed.

In the middle of the audience spectrum training is need to inform the value of social beyond connecting people to people and content, sharing more, and the power of inviting others. For more on value beyond connecting people to people and content see “Solving for building backlash of Enterprise Social Networks” posted by Richie.

At the other end of the audience spectrum are employees who may use social media only occasionally or not at all. These are sometimes (not always) senior management. They may require a bit of handholding, and learning about specific benefits of why they should invest the time to learn something new. They also may be concerned about privacy. There is training needed to trust the platforms, learning the value of connecting to people, and benefiting by searching for and finding content in an entirely new way. This audience will not simply come to the party because they received a flyer, there is personal touch needed.

Sponsorship, they must come from everywhere

Successful deployment of social media (either internally or externally) requires commitment from senior management. However senior managers are unlikely demonstrators of sponsorship for social. Demonstrating sponsorship for social means using it, and many (not all) senior managers lack the time, commitment, and authenticity (don’t take it to heart, being authentic on social is an art, even if you are an inherently authentic person) to truly be social.

Sponsors of social medial must come from all tranches of the organization. The trusted employees, and employees that are opinion leaders can demonstrate sponsorship driving adoption. The trusted must create content, celebrate others, and invite opinion leaders (many times openly). Opinion leaders must share content of others, invite the unlikely senior managers (yes, sometimes openly as well), and advocate for the value of media other than text (such as videos) by using said new media. Finally, senior managers who are seen as unlikely adopters by the masses must be authentic. The unlikely audience should upload photos (authentic photos, not the boring corporate headshots), celebrate the opinion leaders, and share information created by the trusted.

This type of sponsorship and authentic adoption up and down the corporate ladder enables organizations to influence with sponsorship. After all, well attended parties are sponsored.

Design, customize the user experience

Inarguably, social can be separated into the believers, the voyeurs and the nay-sayers. The believers get it, and the current design of social works for them. Empower your believes, celebrate them, and hope that you can challenge them.

The voyeurs are the folks that come to the social platform, look around and leave (people that peek into restaurants or lounges and then keep going). Why do they do this? Many times it is because they “see no value when first logging into a social platform”. For us believes we ask, “really no value?” The fact is voyeurs do not see value when logging in initially, this is because they are not a part of any group, haven’t liked anything, haven’t created any content or commented or shared. Of course they see not value, the initial social experience is empty! Organizations must design social platforms to demonstrate value to voyeurs. We know who said voyeurs are, who they work for and who works for them, their peers constitute their implied social graph. We know what groups their “social graph” are in, what documents and topics their social graphs are interested in, and what questions their social graph have asked and answered. The design of the social platform should suggest a curated environment for the voyeurs on first login based on the activity and preferences of the implied social graph. When a voyeur logs in, if he/she accepts all curated suggestions, he/she will “LEAP” onto the social platform and see immediate value. This is an example of what we mean by enabling adoption with design.

Closing

This conversation can be detailed into a longer discussion, but at the heart of it, adoption is not unsolvable. There is a party happening on the grown up social networks and if no one is coming to the party we have to think like nightclub owners; guide with training, influence with sponsorship and enable a good experience with design.

Content Can’t Take A Vacation (Or Even A Sick Day!) #TLTActiance

Posted by belbey in Actiance, Employee Behavior, Enterprise 2.0, Financial Services, Google, Guest Post, New Internet, Social Networking on January 31, 2013

Today we bring you the first of a new series on the Actiance blog: Thursday’s are “Thought Leader Thursdays” (or #TLTActiance). I’ll preface this by saying that the content is entirely that of our thought leaders, who come from all over the world, the industry and from different areas of business.

Today we bring you the first of a new series on the Actiance blog: Thursday’s are “Thought Leader Thursdays” (or #TLTActiance). I’ll preface this by saying that the content is entirely that of our thought leaders, who come from all over the world, the industry and from different areas of business.

Our inaugural blog comes from our good friend and colleague in the industry, April Rudin, who you may know from @TheRudinGroup. April writes and blogs extensively, in and around the financial services space. She’s well known for her blogging on @huffingtonpost and you’ll see her at most of the financial services events especially on the East Coast of the USA.

Enjoy the blog! Sarah Carter

One of the most frequent financial advisor/wealth manager miscues in social/digital marketing is the lack of a content calendar or a basic marketing plan. It amazes me how the “planners have no plan” when it comes to new client acquisition or retention. Many people approach it almost impulsively, like opening up a Twitter account, without any clue about how to use it, what their messaging should be, or even an avatar/photo! What’s more, this “play” or experimentation is happening on the most visible amplified platform possible: the internet.

Ugh! How can you avoid embarrassing “Social Media Hall of Shame?” In this blog, I will discuss one aspect which is importance of on-going consistent and constant content. While there are plenty of mistakes and faux pas to make, the easiest to avoid is the “content vacation.” To me, this is the most egregious “offense” and it discredits the firm/advisor to existing/potential clients in the worst way: not following through with a plan. Here are a few examples. An advisor opens a Twitter account, begins following friends, or anyone, and has one solo tweet, something like “I am on Twitter now”. That was last January. The Twitter account has sat vacant since. Isn’t it suggesting that the advisor may behave that way with my assets? Another example is the blog which is posted inconsistently, i.e. January, February, March August, November, (you get the idea!). The “Hall of Shame” blog topics are without any thread linking the blog to the firm or to each other, and, perhaps the blogs were part of a one-time newsletter which has never been repeated again.

Ugh! Ugh! Developing a compelling content calendar can be very helpful in staying on track and on-time. To create an actionable, content calendar, you need to determine: What is the content? Who is the audience? Which platforms will be used? And who is responsible for what? Accountability is the key to creating a system, process for the positioning of your personal and firm’s brand on a regular basis in a way which leads back to you, your firm and new/more AUM.

I asked Kathleen Pritchard, Director and Head of Advisor Development for Legg-Mason about the importance of good, consistent content. Kathleen remarked, “While financial advisors may have limited time and resources, it’s the differentiated content which will attract and engage with your audience.”

Kathleen and I both agree that one way to create a compelling content process to include curating content from guest bloggers such as other trusted advisors is one way to “pepper” your blog with interesting stories tied to the calendar. An example would be to calendar a tax attorney to write a “year-end” blog. Inviting other third-party experts will also assist in your outreach as the contributor is likely to send your blog out within their own network as well. Repurposing the same content is another way to help and using evergreen content which is not time-sensitive can be useful in your calendar.

The brevity of this blog and the complexity of this important messaging are at odds. I have so much more to say but limited to 500 characters. Contact me.

April may be contacted via email at april@therudingroup.com or on Twitter @TheRudinGroup

Belbey Blogs: Before you go social, check with Uncle Sam

Posted by belbey in Actiance, Collaboration, Compliance, eDiscovery, Electronically Stored Information (ESI), Employee Behavior, Enterprise 2.0, Enterprise IM, Facebook, Financial Services, FINRA, Guest Post, Legal, Social Networking, Unified Communications, Web 2.0 on January 30, 2013

Today’s post is a collaboration between Richie Etwaru, Director, UBS and Joanna Belbey, Social Media and Compliance Specialist, Actiance

Today’s post is a collaboration between Richie Etwaru, Director, UBS and Joanna Belbey, Social Media and Compliance Specialist, Actiance

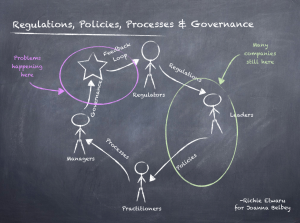

It’s difficult to debate the value of installing enterprise social networks.

Richie Etwaru, a futurist and avid speaker, covered the current state, business value, and future thinking needed around the construct of what he phrases the #ENTSOCNET (an internal enterprise social network). Mr. Etwaru titled the piece Solving for building backlash of Enterprise Social Networks and covers the 1st, 2nd and 3rd generation of the #ENTSOCNET. Installing an internal social network, driving, adoption and extracting business value as Mr. Etwaru describes, is complicated and difficult work. Leaders must ensure that said complicated and difficult work is being done under the auspices of regulatory guidelines.

There are regulatory compliance, corporate governance, and legal requirements organizations must address before deploying social. There however, is an impedance mismatch and some amount of misinterpretation between what the regulators consider enterprise social media, and what leaders in the enterprise consider to be enterprise social media. The spirit of the regulations suggest that whether an enterprise in installing an internal social network (what Mr. Etwaru describes as the #ENTSOCNET) for its employees only, or leveraging external social networks such as Facebook, LinkedIn or Twitter; all communications, messages, inboxes, comments, endorsements, DMs, tweets retweets etc. are governed under the regulations.

What Regulators want

More than 2 years ago, regulators of the securities industries began to issue guidance on how to use social media. The Financial Industry Regulatory Authority (FINRA), The Securities and Exchange Commission (SEC), Investment Industry Regulatory Organization of Canada (IIROC), National Association of Insurance Commissioners (NAIC) and others view social media, whether it’s external or internal, as just another form of business communications, such as email or instant messages. They remind us that it’s the content that is determinative, not the platform. Regulators also expect that firms demonstrate that they are supervising, or reviewing, a pre-defined portion of these communications. Other more general legislation may also apply such as Sarbanes-Oxley (SOX) Gramm-Leach-Bliley Act, and the data breach notification laws (PCI, DSS).

What this all means

In short, whether internal or external, firms need to ensure that all business communications (or “business as such”) are captured, archived, supervised and made easily e-discoverable. There is nothing new here as this has been an evolution. First paper, then email, instant messages, now both internal and external social media, firms continue to be challenged to capture, retain and review a portion of all business records in whatever form they appear. As a first step, firms may use their existing email and instant message retention policies as a framework to develop policies for internal and external social media. Governing said policies is a separate and pronounced challenge.

Governance is key

Firms are increasingly committed to comprehensive corporate governance to avoid scandal and to comply with regulations. The development of sound policies and procedures before deployment is key, given the vast amount of data stored in most collaboration environments and the free ranging conversations among employees, contractors and even clients that can ensue, policies must be defined.

Specifically policies should address: records management (retention, litigation readiness, privacy), information management (making sure that records are tamper proof, and easily accessible), data deposition (disposal of data) and conflict management. Where possible, firms should automate policies with technology to protect their intellectual property, prevent the creation and distribution of inappropriate content and provide an audit trail of all activity to ensure accountability.

It’s a serious legal matter

When learning of pending litigation, firms must be able to preserve all records (“legal hold” or “ligation holds”) that may relate to legal action against the company, including records of social activity. According to the Federal Rules of Civil Procedures (FRCP), firms must meet discovery requests for paper as well as electronic documents (spreadsheets, slide decks), emails, posts, and conversations across social media in a timely fashion. Therefore, firms need plans and the means to retain and produce such data upon request. Email was new and difficult, social is not yet understood, complex and mindboggling.

Social, not my grandma’s email

Social media, due to its nature, adds complexity to these requirements as interactions occur over time. For example, a blog starts with an initial post, then readers may add comments, or change their minds and revise and delete their comments and the original author may respond. These interactions could go on for months in some cases. Firms should have the ability to produce all of these threads of posts, comments and replies “in context” to give meaning to the conversations. By providing context, firms may reduce litigation costs by reducing the number of hours required by attorneys to sort through records to determine the sequence of events and the true essence of the conversations. Preserving context requires intelligent software solutions.

What now

Enterprise-wide “social business” tools were designed to facilitate collaboration, not necessarily to meet the legal and compliance requirements of regulated firms or public corporations. They offer basic functionality to capture and archive communications, but not the reporting, contextual view of information, nor granular policy setting that may be desired. Firms are therefore advised that before deploying enterprise wide collaboration tools, they look to third party vendors to ensure their compliance requirements are met.

Collaboration, no pun intended

I reached out to Mr. Etwaru (whom I met a few years ago at a conference in NYC) and shared this perspective. His response is below.

~~~~~~~~~~~~~~~~~~~~~

Hi Joanna,

Your thoughts are spot on. From the regulators (who are doing a great job) point of view social, email, chat, etc. all carry similar risk and hence are metaphorically bucketed from a guidance standpoint. In the enterprise however, the risk with social is multiples higher for a multitude of reasons. One reason is employees learned of social in their personal lives where regulations are by and large absent. Hence, when using social in the enterprise (or in a commercial manner) employees (fallible as we are) tend to assume the same “free range” comes with social. The policy, governance and education you suggested is paramount, I could not agree more.

That being said …

However daunting all of this may be, the biggest risk is not using internal social media to break down silos and to unleash the intellectual power of the enterprise while driving innovation.

BTW, love your diagram, I can help you make it pretty

Hope this helps,

-R

~~~~~~~~~~~~~~~~~~~~~

Diagram above rendered by Mr. Etwaru,

-Joanna

Belbey Blogs: New Guidance on Using Social Media at Retail Banks

Posted by belbey in Actiance, Collaboration, Compliance, eDiscovery, Electronically Stored Information (ESI), Employee Behavior, Enterprise 2.0, Enterprise IM, FFIEC, Financial Services, FINRA, Legal, Malware, Privacy, Retail banking on January 25, 2013

This week, the Federal Financial Institutions Examination Council (FFIEC) released “Social Media: Consumer Compliance Risk Management Guidance. The FFIEC is asking for comments within sixty days. You can download the 31-page document here.

Its release has created quite a stir within the banking industry. A comprehensive article appeared on TheFinancialBrand.com, “Regulatory Shocker on Social Media in Banking Coming Soon” that summarizes the guidance quite nicely.

But . . . what’s so shocking?

We’ve been having the same conversations in the securities industry for three years. And in those three years, firms have learned that there are three major areas of risk that need to be mitigated before deploying social media:

- Security: your IT department needs to prevent your firm’s proprietary and client information from being leaked out either inadvertently or maliciously from the enterprise. They also need to ramp up malware protection. That’s because social media users are susceptible to incoming threats as they view themselves as part of a tribe and tend to click on any link sent by a “friend.”

- Compliance and Governance: your legal and compliance departments already know that there are thousands of rules and regulations that govern the communications and advertising of publicly held corporations, firms in general, and bank specifically. Take the securities industry as an example – the banking regulators aren’t issuing new rules and regulations around social media. Social media is viewed as just another form of written communications. Your compliance department is therefore challenged to interpret existing rules as they apply to social media and to develop and enforce firm policies.

- Enablement: your executive team is concerned about productivity and the bottom line. Now that every employee can be the face of the business, you either have a powerful marketing tool or your worst nightmare. Employees will need to be trained on how to use social media effectively to meet the firm’s goals, such as nurturing existing clients, attracting new business, recruiting, and brand awareness.

However, during the last three years, we’ve learned that all these risks can be mitigated by strong corporate polices, backed up with technology and training.

So far, so good. Nothing new here. Or is there? In addition to what we’ve already seen from other regulators, the FFIEC specifically also calls for:

- Creation of policies to address negative feedback or customer complaints, even if a financial firm chooses not to actively engage in social media.

- Monitoring to protect the firm’s brand identity

- Due diligence and oversight for third-party vendors that firms may hire in connection with social media

And the one that I find most interesting:

- Processes and reporting to demonstrate how social media “contributes to the strategic goals of the institution.”

In other words, the FFIEC recommends that firms measure the ROI of social media.

It will be interesting to see the reaction that FFIEC gets from the industry. I just hope that the banking industry can use some of the key learnings from the securities industry to streamline the processes to reap the benefits of “getting social.”

For more details on how to deploy social media within retail banking, you can also check out Belbey Blogs: Upcoming Guidance for the Use of Social Media for Retail Banking from FFIEC.

Facebook Graph: The Supermarket Coupon Book of Social Selling

Posted by ASocialNomad in Actiance, Employee Behavior, Facebook, Financial Services, FINRA, Social Networking on January 16, 2013

You can’t possibly have missed that yesterday, Facebook made a big announcement, with the news that Facebook Graph is to hit our social inbox in the very near future. Here at Actiance, our financial services customers who use social focus to a large extent on LinkedIn as their primary network. Asking as to why, there are a variety of answers:

- It’s viewed as the “professional network”

- There are less concerns about “more personal” content being shared

- It’s pretty much where their customers are.

I don’t disagree with what’s written above, but actually I think Facebook and Financial Services were made for each other. I fundamentally don’t think that I can separate the professional Sarah from the personal Sarah. I’m very Gen Y in my thinking like that (actually I’m still 17 years old in my head, despite what the wrinkles around my eyes tell you). And for that reason, I have got over my concern that my colleagues, work acquaintances and customers might see something about my personal life through any of my social networks. As I say as I begin each demo of Socialite, our social engagement solution – you may see something inappropriate from my friends, family or colleagues, but you’re all adults.

Facebook gives me a different relationship with folks than LinkedIn. Would I know of the foodie habits of one head of compliance? or the horse riding antics of a Gartner analyst? or the movie mania of @AugieRay if I didn’t have Facebook? More than likely not.

Transpose this specifically to financial services. We – and that’s the Royal we – share so much of our lives on Facebook, that it actually complements the provision of financial services products. It allows more suitable product to be provided to us – and suitable product provisions are a key tenet of regulators such as FINRA. It allows us to actually connect more as human beings, we’re social animals, and have been for eons. The transparency of Facebook is perhaps what worries us, but you know, we’ll get over that as we become more social in the virtual world.

So, and yes there is a point to this blog. While the complete functionality of Facebook Graph is yet to be revealed, and we look forward to the beta, its one more step towards being able to use the information that we all so readily share to work towards social selling. I look at it as the supermarket coupon book of social. You have my shopping habits down pat, so provide me with more suitable product. @Safeway has my number in this regard, so why not my Financial Services provider?

So, and yes there is a point to this blog. While the complete functionality of Facebook Graph is yet to be revealed, and we look forward to the beta, its one more step towards being able to use the information that we all so readily share to work towards social selling. I look at it as the supermarket coupon book of social. You have my shopping habits down pat, so provide me with more suitable product. @Safeway has my number in this regard, so why not my Financial Services provider?