Archive for category Guest Post

Transaction banking is the ‘new’ sexy #TLTActiance

Posted by belbey in Actiance, Banking, Financial Services, Guest Post, iPhone, iPod, Mobile, New Internet, Retail banking, Trends on April 25, 2013

This Thursday’s Thought Leader Actiance (#TLTActiance) guest blog is by Elizabeth Lumley, special projects editor at financial services newswire Finextra, based in London. Follow her on Twitter @LizLum

According to research from the Boston Consulting Group, revenues from global transaction banking are expected to grow from $189 billion in 2011 to $509 billion in 2021 – an increase of 170%.

This renewed focus on the transaction bank has brought up several key trends. To highlight these I’m going to look at two trends from Finextra’s Global Banking Transaction Survey.

Most banks are combining cash management, payments, trade finance (and sometimes securities services) into one business unit.

Almost 90% of the banks surveyed in 2012 have created a transaction banking group, combining these business, or plan to in the near future. That number has grown exponentially. In 2010, 57% of those surveyed had merged, or were planning to merge, their trade finance and cash management business. That rose to 77% in 2011.

Now, there are a few issues I have with these statistics. And it’s from a technical, rather than a business strategy standpoint.

The client-facing sides of the bank are now concerned with this idea of ‘customer-centricity’. Banks need a ‘customer view’ of their services, not a product-view of their services. Why?

So that banks can enable a stronger strategic focus on customer service, channel and product innovation. So that banks can ‘cross-sell’ their services. It is not a giant leap to suggest to a cash management client, that ‘oh by the way…we also offer supply chain.’

However, saying that a bank is now ‘customer-focused’ rather than product-focused, is very different from re-engineering decade’s old, legacy-heavy, enterprise-wide infrastructure that has been aligned along product lines.

Piecing together your old ‘product’ systems with some dodgy middleware, sticky tape and chewing gum, or moving your cash management guys to the same floor of the building as your trade finance gals – does not mean you are now operating in a serene, holistic, IT paradise (complete with angels and cotton candy.)

In 2013, most banks ‘want’ to combine their business under the neatly packaged ‘transaction banking’ umbrella – because of all the reasons cited including ‘better press’. (I mean who will admit, to the media, that their business is struggling to cope with changes in customer behaviour; with ageing systems that were probably built when people thought having a phone in your car was the height of innovation?)

But many banks are still struggling with real issues concerning complexity their IT environments. In fact 57 per cent of respondents, to the survey, said IT and system complexity is a hindrance. Any business within the bank, can offer cool, smart, innovative products – but if the infrastructure supporting them is, for lack of a better word…creaky, then the whole house of cards will fall apart.

Mobile channel development is a growing trend, with 45 per cent of banks ranking this a priority in the coming year, while 63 per cent said expanding self-service channels such as mobile would be part of their strategy over the next three years.

Conservative IT people – and let’s face it most bank IT people aren’t your young guns in hipster jeans and retro glasses (not that I’m saying that’s a bad thing) – tend to deal with innovation in terms of ‘products’. The digital revolution that has been going on around us, in the consumer world, is often seen in banking as a mobile revolution.

The questions that are being asked in innovation and development teams right now are:

- How do you get payments on the phone?

- How do you engineer a ‘Wallet’ on the phone?

- How do you allow a corporate treasurer to authorise a payment on the phone?

This is the ‘mobile as a channel’ view of the world – which has led many banks to make the mistake of trying to shove the online banking experience into the mobile. (Or to shove the card onto the phone via NFC)

You should not think of mobile as a channel, but think of it as the channel. Whether you’re a retail customer or a corporate customer – you’re not looking for banking services ‘on a mobile’ you are looking for ‘mobile banking services.’ There’s a difference.

The cell phone, tablet or smart phone is merely the device of today.

According to last year’s Capgemini World Payments Report only two percent of mobile phone users have ever made a payment using their phone. Customers are not crying out for more apps – where they are moving towards is being able to access banking and payments services wherever they are.

It is people who are mobile. If your innovation strategy is bogged down with the device – it will move in the wrong direction.

That revolution in consumer banking is having an immediate impact on what corporate customers are demanding from their banks and how banks plan on focusing their investment in innovation.

Elizabeth Lumley is a global specialist commentator on services, regulations, risk, data and technology in investment, retail, and global transactional banking. She is an internationally recognised reporter, tweeter, blogger and broadcast journalist. Elizabeth Lumley is currently special projects editor at financial services newswire Finextra, based in London, where she is responsible for all the multi-media output.

Advisor View: I Believe in Social Media!

Posted by actiance in Financial Services, Guest Post, personal v professional, Social Networking on February 21, 2013

This week’s thought leader Thursday commentary comes from Kim Gaxiola,CFP®, AAMS, Financial Advisor, speaker, educator, and founder of TechGirl Financial. As a big fan of women in technology, Kim’s mission is to provide Silicon Valley with financial education that makes professionals and employees more comfortable making important financial decisions. She has over 10 years of experience as a financial advisor, 15 years in the financial services industry, and a bachelor’s degree in economics from the University of California, Los Angeles (UCLA).

If my husband Victor told me 2 years ago that I was going to have my own blog, and actually enjoy writing articles, posting them on social media, and seeing the response I was going to generate from it, I would have said NO WAY. I have enough to do just managing my practice. Why do I need to write articles, and then tweet, like them, or pass on LinkedIn? I could just pass around others good content.

If my husband Victor told me 2 years ago that I was going to have my own blog, and actually enjoy writing articles, posting them on social media, and seeing the response I was going to generate from it, I would have said NO WAY. I have enough to do just managing my practice. Why do I need to write articles, and then tweet, like them, or pass on LinkedIn? I could just pass around others good content.

It pains me to say it, but he was right! As you can see from this article itself, I am not known for my writing. When I started my new website www.techgirlfinancial.com and included a blog component, I slowly started to include my own material, along with the marketing material I purchased or found on the web. After writing a couple articles and shamelessly promoting them on Facebook, Twitter, and LinkedIn, I have grown to like this aspect of my business. I have found that is very fun to write and get noticed as an authority when it comes to things having to do with personal financial planning and other matters. It is amazing to see how I can reach out to people near and far simply by telling a story and then sharing it using social media.

My website is my unique place to bring content and ideas on topics having to do with financial planning or my niche market, women in technology. My profiles on LinkedIn, Twitter, and Facebook are my amplifiers. It is my voice and my interests that are being shared across the country to my unique audience of women that I like to work with. This is the new medium that delivers the right content to the right audience, and they are looking for your message. If you are not out there telling it to them, they are finding it from someone else. Who do you want them to see, you or someone else?

It is so fascinating to see the “likes” or the activity and “comments” generated from the different posts and material I provide. We don’t always know what resonates with our clients and prospects. The geeky financial articles on the markets are fascinating to me, but they aren’t always what resonate with my clients. Using social media helps me identify those aspects that are more important or interesting to clients and prospects as well. That allows me to send a message and identify with them on a more personal note.

In addition to telling, it’s extremely fun to sit back and listen. Our business is all about helping families reach their goals. This is the core of what individuals are sharing with their friends on Facebook. You will have a much quicker ability to react to life changes when you see them posting on Facebook, then if you were to wait around for them to call you. That’s IF they call you. As I listen and see photos of my clients as they report about the birth of a baby or grandchild, a new job, a wedding, etc…it is with great pleasure that I can witness these happy events with them, and make sure that the proper planning steps are being done at those key life events. There is much to worry or stress about in our business. But this is not it. This is a place where our relationships with our clients can become so much deeper. If you’re not taking advantage of that, you may be missing out. More important, someone else may be listening and connecting on a more personal note than you.

Kim Gaxiola may be reached at (800) 584.3652 or kim@gaxiolafinancialgroup.com or www.techgirlfinancial.com.

TechGirl Financial is a part of Gaxiola Financial Group. Registered representative, securities offered through Cambridge Investment Research, Inc., broker-dealer, member FINRA/SIPC. Investment advisor representative, Cambridge Investment Research Advisors, Inc., a registered investment advisor. Cambridge and Gaxiola Financial Group are not affiliated. Gaxiola Financial Group | 305 Vineyard Town Center #369 | Morgan Hill, CA 95037Content Can’t Take A Vacation (Or Even A Sick Day!) #TLTActiance

Posted by belbey in Actiance, Employee Behavior, Enterprise 2.0, Financial Services, Google, Guest Post, New Internet, Social Networking on January 31, 2013

Today we bring you the first of a new series on the Actiance blog: Thursday’s are “Thought Leader Thursdays” (or #TLTActiance). I’ll preface this by saying that the content is entirely that of our thought leaders, who come from all over the world, the industry and from different areas of business.

Today we bring you the first of a new series on the Actiance blog: Thursday’s are “Thought Leader Thursdays” (or #TLTActiance). I’ll preface this by saying that the content is entirely that of our thought leaders, who come from all over the world, the industry and from different areas of business.

Our inaugural blog comes from our good friend and colleague in the industry, April Rudin, who you may know from @TheRudinGroup. April writes and blogs extensively, in and around the financial services space. She’s well known for her blogging on @huffingtonpost and you’ll see her at most of the financial services events especially on the East Coast of the USA.

Enjoy the blog! Sarah Carter

One of the most frequent financial advisor/wealth manager miscues in social/digital marketing is the lack of a content calendar or a basic marketing plan. It amazes me how the “planners have no plan” when it comes to new client acquisition or retention. Many people approach it almost impulsively, like opening up a Twitter account, without any clue about how to use it, what their messaging should be, or even an avatar/photo! What’s more, this “play” or experimentation is happening on the most visible amplified platform possible: the internet.

Ugh! How can you avoid embarrassing “Social Media Hall of Shame?” In this blog, I will discuss one aspect which is importance of on-going consistent and constant content. While there are plenty of mistakes and faux pas to make, the easiest to avoid is the “content vacation.” To me, this is the most egregious “offense” and it discredits the firm/advisor to existing/potential clients in the worst way: not following through with a plan. Here are a few examples. An advisor opens a Twitter account, begins following friends, or anyone, and has one solo tweet, something like “I am on Twitter now”. That was last January. The Twitter account has sat vacant since. Isn’t it suggesting that the advisor may behave that way with my assets? Another example is the blog which is posted inconsistently, i.e. January, February, March August, November, (you get the idea!). The “Hall of Shame” blog topics are without any thread linking the blog to the firm or to each other, and, perhaps the blogs were part of a one-time newsletter which has never been repeated again.

Ugh! Ugh! Developing a compelling content calendar can be very helpful in staying on track and on-time. To create an actionable, content calendar, you need to determine: What is the content? Who is the audience? Which platforms will be used? And who is responsible for what? Accountability is the key to creating a system, process for the positioning of your personal and firm’s brand on a regular basis in a way which leads back to you, your firm and new/more AUM.

I asked Kathleen Pritchard, Director and Head of Advisor Development for Legg-Mason about the importance of good, consistent content. Kathleen remarked, “While financial advisors may have limited time and resources, it’s the differentiated content which will attract and engage with your audience.”

Kathleen and I both agree that one way to create a compelling content process to include curating content from guest bloggers such as other trusted advisors is one way to “pepper” your blog with interesting stories tied to the calendar. An example would be to calendar a tax attorney to write a “year-end” blog. Inviting other third-party experts will also assist in your outreach as the contributor is likely to send your blog out within their own network as well. Repurposing the same content is another way to help and using evergreen content which is not time-sensitive can be useful in your calendar.

The brevity of this blog and the complexity of this important messaging are at odds. I have so much more to say but limited to 500 characters. Contact me.

April may be contacted via email at april@therudingroup.com or on Twitter @TheRudinGroup

Belbey Blogs: Before you go social, check with Uncle Sam

Posted by belbey in Actiance, Collaboration, Compliance, eDiscovery, Electronically Stored Information (ESI), Employee Behavior, Enterprise 2.0, Enterprise IM, Facebook, Financial Services, FINRA, Guest Post, Legal, Social Networking, Unified Communications, Web 2.0 on January 30, 2013

Today’s post is a collaboration between Richie Etwaru, Director, UBS and Joanna Belbey, Social Media and Compliance Specialist, Actiance

Today’s post is a collaboration between Richie Etwaru, Director, UBS and Joanna Belbey, Social Media and Compliance Specialist, Actiance

It’s difficult to debate the value of installing enterprise social networks.

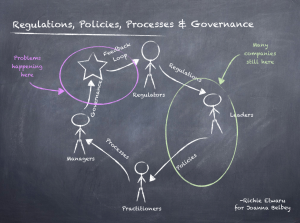

Richie Etwaru, a futurist and avid speaker, covered the current state, business value, and future thinking needed around the construct of what he phrases the #ENTSOCNET (an internal enterprise social network). Mr. Etwaru titled the piece Solving for building backlash of Enterprise Social Networks and covers the 1st, 2nd and 3rd generation of the #ENTSOCNET. Installing an internal social network, driving, adoption and extracting business value as Mr. Etwaru describes, is complicated and difficult work. Leaders must ensure that said complicated and difficult work is being done under the auspices of regulatory guidelines.

There are regulatory compliance, corporate governance, and legal requirements organizations must address before deploying social. There however, is an impedance mismatch and some amount of misinterpretation between what the regulators consider enterprise social media, and what leaders in the enterprise consider to be enterprise social media. The spirit of the regulations suggest that whether an enterprise in installing an internal social network (what Mr. Etwaru describes as the #ENTSOCNET) for its employees only, or leveraging external social networks such as Facebook, LinkedIn or Twitter; all communications, messages, inboxes, comments, endorsements, DMs, tweets retweets etc. are governed under the regulations.

What Regulators want

More than 2 years ago, regulators of the securities industries began to issue guidance on how to use social media. The Financial Industry Regulatory Authority (FINRA), The Securities and Exchange Commission (SEC), Investment Industry Regulatory Organization of Canada (IIROC), National Association of Insurance Commissioners (NAIC) and others view social media, whether it’s external or internal, as just another form of business communications, such as email or instant messages. They remind us that it’s the content that is determinative, not the platform. Regulators also expect that firms demonstrate that they are supervising, or reviewing, a pre-defined portion of these communications. Other more general legislation may also apply such as Sarbanes-Oxley (SOX) Gramm-Leach-Bliley Act, and the data breach notification laws (PCI, DSS).

What this all means

In short, whether internal or external, firms need to ensure that all business communications (or “business as such”) are captured, archived, supervised and made easily e-discoverable. There is nothing new here as this has been an evolution. First paper, then email, instant messages, now both internal and external social media, firms continue to be challenged to capture, retain and review a portion of all business records in whatever form they appear. As a first step, firms may use their existing email and instant message retention policies as a framework to develop policies for internal and external social media. Governing said policies is a separate and pronounced challenge.

Governance is key

Firms are increasingly committed to comprehensive corporate governance to avoid scandal and to comply with regulations. The development of sound policies and procedures before deployment is key, given the vast amount of data stored in most collaboration environments and the free ranging conversations among employees, contractors and even clients that can ensue, policies must be defined.

Specifically policies should address: records management (retention, litigation readiness, privacy), information management (making sure that records are tamper proof, and easily accessible), data deposition (disposal of data) and conflict management. Where possible, firms should automate policies with technology to protect their intellectual property, prevent the creation and distribution of inappropriate content and provide an audit trail of all activity to ensure accountability.

It’s a serious legal matter

When learning of pending litigation, firms must be able to preserve all records (“legal hold” or “ligation holds”) that may relate to legal action against the company, including records of social activity. According to the Federal Rules of Civil Procedures (FRCP), firms must meet discovery requests for paper as well as electronic documents (spreadsheets, slide decks), emails, posts, and conversations across social media in a timely fashion. Therefore, firms need plans and the means to retain and produce such data upon request. Email was new and difficult, social is not yet understood, complex and mindboggling.

Social, not my grandma’s email

Social media, due to its nature, adds complexity to these requirements as interactions occur over time. For example, a blog starts with an initial post, then readers may add comments, or change their minds and revise and delete their comments and the original author may respond. These interactions could go on for months in some cases. Firms should have the ability to produce all of these threads of posts, comments and replies “in context” to give meaning to the conversations. By providing context, firms may reduce litigation costs by reducing the number of hours required by attorneys to sort through records to determine the sequence of events and the true essence of the conversations. Preserving context requires intelligent software solutions.

What now

Enterprise-wide “social business” tools were designed to facilitate collaboration, not necessarily to meet the legal and compliance requirements of regulated firms or public corporations. They offer basic functionality to capture and archive communications, but not the reporting, contextual view of information, nor granular policy setting that may be desired. Firms are therefore advised that before deploying enterprise wide collaboration tools, they look to third party vendors to ensure their compliance requirements are met.

Collaboration, no pun intended

I reached out to Mr. Etwaru (whom I met a few years ago at a conference in NYC) and shared this perspective. His response is below.

~~~~~~~~~~~~~~~~~~~~~

Hi Joanna,

Your thoughts are spot on. From the regulators (who are doing a great job) point of view social, email, chat, etc. all carry similar risk and hence are metaphorically bucketed from a guidance standpoint. In the enterprise however, the risk with social is multiples higher for a multitude of reasons. One reason is employees learned of social in their personal lives where regulations are by and large absent. Hence, when using social in the enterprise (or in a commercial manner) employees (fallible as we are) tend to assume the same “free range” comes with social. The policy, governance and education you suggested is paramount, I could not agree more.

That being said …

However daunting all of this may be, the biggest risk is not using internal social media to break down silos and to unleash the intellectual power of the enterprise while driving innovation.

BTW, love your diagram, I can help you make it pretty

Hope this helps,

-R

~~~~~~~~~~~~~~~~~~~~~

Diagram above rendered by Mr. Etwaru,

-Joanna

Superstorm Sandy, #GivingTuesday and BDI’s Financial Services Social Communications Event

Posted by Victor Gaxiola in Conference, Guest Post, Social Networking on January 2, 2013

Today’s post comes from Joyce Sullivan, CEO of SocMediaFin, a social media consulting firm for financial services, specialty firms and industry executives. Joyce can be found on LinkedIn, Facebook, Twitter and on her website SocMediaFin.

As someone who considers herself lucky to have survived Superstorm Sandy, by only losing electrical power for six days – very thankful all our trees stayed in place – I decided to attend one of my favorite social media and financial services events of the year.

As someone who considers herself lucky to have survived Superstorm Sandy, by only losing electrical power for six days – very thankful all our trees stayed in place – I decided to attend one of my favorite social media and financial services events of the year.

I’m talking about the Business Development Institute’s annual Financial Services Social Communications 2012: Case Studies and Roundtables event held on November 15, 2012.

Though I have attended many BDI events, this one was particularly special as it was the first BDI event after #Sandy, and because the President of the Financial Women’s Association (FWA) would be on stage introducing one of my favorite social media mavens.

As a long-time FWA member, I was especially proud to hear, FWA President Susan Harper, who is also Director and attorney at, The Bates Group LLC, speak to this illustrious group of financial services executives about the FWA’s mission and vision. And to round out the FWA proud-ness factor, President Harper introduced Joanna Belbey, social media expert and speaker for Actiance, and FWA member, too.

As readers of this column know, Joanna Belbey is the author of Belbey Blogs where she shares her observations on social media, regulatory and compliance guidance for financial firms.

As Joanna took the stage, and before launching into her talk, she asked the audience to take her picture and tweet with #GivingTuesday in their message. As many of my twitter followers know, I enjoy taking pictures ~ from the front row, always – and tweeting at events. I too, along with the audience, snapped pictures and tweeted at Joanna’s suggestion.

Since there were so many lovely pictures and tweets about this initiative, I decided to Storify it. What is #GivingTuesday and Storify, you may ask? See the tweets and pictures here to find out > http://bit.ly/BelbeyBDIGivingTuesday.

Following Joanna’s talk, many speakers graced the stage and gave us thought-provoking analyses and trends on social media and financial services. There was plenty of time for the audience to engage with the speakers through the roundtable discussion that followed.

If you haven’t yet attended a BDI event, you may want to get your 2013 resolutions list started early by adding an event to attend. http://bit.ly/BDICalendarofEvents

Give me a shout out on twitter @JoyceMSullivan to let me know when I’ll see you at an upcoming event. I look forward to meeting you virtually and IRL, as we say, though my social media colleagues tell me that virtual, is now, real life, too.

Joyce Sullivan is founder and CEO of SocMediaFin, a social media consulting firm for financial services, specialty firms and industry executives. With over 20 years experience as Vice President with firms including, Citi, Credit Suisse, JPMorgan Chase, and Wells Fargo/First Fidelity, Ms. Sullivan brings a seasoned industry perspective to the emerging world of social media. As an advisory board member of the Financial Women’s Association, she serves as their Chief Digital Strategist. Ms. Sullivan holds an MBA from the Zicklin School of Business, Baruch College, City University of NY in International Finance and Marketing, a BA in Education from University of Saint Joseph, Connecticut, and the Project Management Professional (PMP) designation from the Project Management Institute.